A residential heating solid biofuels market state of the art was carried within Task 2.1. The report is composed of 4 parts: market state of the art, statistical report of the market, SWOT analyses, and a report with the conclusions of a survey made to final users to study the public acceptance of the studied biofuels.

A residential heating solid biofuels market state of the art was carried within Task 2.1. The report is composed of 4 parts: market state of the art, statistical report of the market, SWOT analyses, and a report with the conclusions of a survey made to final users to study the public acceptance of the studied biofuels.

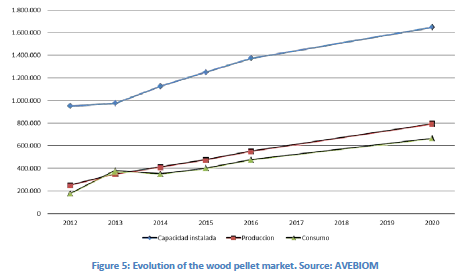

The full report can be downloaded from the following link

The national market study scope comprises for each country: identification of the importance of the residential heating biofuels market in the context of the national energy demand and the bioenergy market, the biomass resources available for relevant biofuels production in each country, the residential heating biofuels production and biofuels use and market prices, the main biofuels chains description, the related legislation and market support measures and relevant information of the most representative national market stakeholders. The market studies were confectioned by the partners AIEL, TUBITAK, CBE, CERTH, ZEZ and GIS, for Italy, Turkey, Portugal, Greece, Croatia and Slovenia, respectively. AVEBIOM and CIEMAT carried out the market study jointly for Spain. Also, AVEBIOM and CIEMAT elaborated the templates of the questionnaires for the rest partners to collect the required information.

A SWOT analysis was also carried out for the main biofuels groups: olive stones, wood chips, dry fruit shells, olive tree prunings and vineyard pruning for every country and then a consolidated version based on the common issues was made.

Also a survey to search the public acceptance of the studied biofuels was delivered to final users in each country.

In the following paragraphs, a small conclusion from every country of the consortium can be found.

Croatia

In Croatia biomass accounts for approximately 11% of the total primary energy supply, while the majority of wood fuel is consumed in households for heating and 95% of produced biomass quantities is exported.

Exploitation of forest and wood biomass for energy has a long tradition in Croatia, especially fire wood and wood residue. Firewood is used by almost all of the households that reported biomass consumption. A very small number of households (4%) use pellets and briquettes or some other type of biomass (mainly tree prunings). Less than half of the population (47%) use some type of biomass for space heating, cooking or water heating in Croatia. This percentage is much higher in rural areas, where approximately three fourths of the households (73%) reported to use biomass for their daily needs, while, on the other hand, the percentage is significantly lower in urban areas (28%).

Wood-based fuels used in Croatia are listed below:

Pellets – most widespread modern wood fuel formed by pressing or crushing of sawdust coarse wood waste or wood chips. A dozen Croatian pellet manufacturers export up to 95% of their products, around 250.000 tons per year.

Briquettes – preceded the popular pellets and it was used by eco-conscious customers, because of small difference in price compared to traditional wood fuel.

Firewood – traditional commercial measures for firewood in Croatia is a cubic meter, and it consists of logs, one meter in length and eight to fifteen centimeters in diameter. Best raw materials for firewood are considered hornbeam, followed by beech and other hardwoods.

Wood chips – used for fuel in large industrial heating or production electricity, with a higher percentage of moisture required in a specially constructed boiler.

Greece

The biomass market study for Greece, performed by CERTH, highlighted the fact that even though biomass is the RES with the highest share in the national primary energy consumption, the per capita consumption of solid biofuels is one of the lowest in the EU-28. In recent years, more than 80% of the bioenergy consumption in Greece is in the residential sector. The main solid biofuels currently utilized for domestic heating are the following:

• Firewood is the main solid biofuel used by Greek households, amounting to 23.8 % of the total thermal energy consumption in the heating period of 2011 – 2012 according to Hellenic Statistical Authority (ELSTAT). The main sources of firewood are non-coniferous forests (968,000 m3 in 2014), imports (around 216,000 m3 in 2014) and firewood from agricultural holdings (more than 460,000 tons in 2010).

• Wood pellets are a growing sector since 2011, but the use level is still behind the levels of other Mediterranean countries such as Spain and Italy. The total annual consumption of wood pellets in the residential sector is estimated by CERTH to be in the range of 50,000 – 65,000 t.

• Agro-industrial residues from olive oil processing is an important biomass source, especially in southern Greece. The usual fuel found on the market is a mixed fraction of olive stones and exhausted olive cake, produced by pomace mills. The Association of Olive Kernel Oil Producers of Greece estimates that for an “average” olive oil yield year around 135,000 t of such mixed fractions are available on the market. Part of this quantity is used for domestic heating. Separation of olive stones from the pulp takes place only in a small number of facilities.

• Nut shells are produced by nut crushing plants and used as fuel locally. The total annual production of nut shells is estimated by CERTH to be below 15,000 t, the majority of which is almond shells. Part of this quantity is used in the residential sector, especially in rural areas.

For solid biofuels already in the market, there is a need to promote awareness regarding fuel quality and best practices for their use, not only among the general public but also among fuel producers.

Olive tree and vineyard prunings represent a large potential biomass source in Greece (the technical potential is estimated by CERTH to between 1.5 to 2.5 million tons dry matter), which is currently unutilized. The promotion of concepts and business models for their effective mobilization is a key element to make these biomass types available on the market.

Italy

The growing of the sector is carried by the low price of biofuels and a rising awareness of the people who are starting to understand the global warming problem and the advantages of using renewables. The central government and local administrations are starting to respond, guided by EU, in terms of wise politics, rewarding high quality biofuels and high energy efficiency for new installations.

The gross Final Energy Consumption in Italy is Around 120 Mtoes in 2015 (Source: GSE, Eurostat 2016). About this consumption thermal energy count more than 50%, of which biofuels consumptions are around 6.52 Mtoes in 2014 (Source GSE, 2015). This consumption makes Italy the 4th bioheat consumer by using biomass within the EU28 area, representing the 9% of the total consumption.

The most of the bioheat consumption, 97% in 2014, goes to residential users, indeed Italy is the EU most important residential market for biomass sector in EU. The main drivers are the installed biomass stoves (more than 5 million) and new installations, that are revamping the current market and increasing the share of biomass by replacing the fossil fuelled devices.

Wood biomass represents most of solid biofuels commercialized in Italy, counting over 20.000.000 tonnes/year. The most common one is wood logs, whose consumption reaches 18.000.000 tonnes/year, while pellet goes around 3.000.000 tonnes/year.

For what concern typical Mediterranean biofuels, the market is not established yet, despite of the huge potential of those products. The current consumption is actually hard to estimate, and the most updated estimations are 90.000 tDM/y for agricultural chips (most from vineyard and olive), 40.000 for olive stone, 140.000 tDM/y for exhausted olive cake and 90.000 tDM/y for nutshells. Together those Mediterranean biofuels interests around 360.000 tDM/y. That’s an interesting value, especially considering that those biofuels are generally by-products.

Portugal

Solid biofuels market, based on controlled biomass and modern and efficient systems, has a great potential of development in Portugal. However, Portugal still has much to do to reach a state of maturity in this market.

Wood (firewood, wood chips, pellets and briquettes) represents about 94% of the total solid biofuels produced in the country, according to the available statistical data. Olive stones and olive cake are used directly as fuel in industries for a long time ago, but the demand for olive stones on the residential and services market is increasing. Nut shells available are typically consumed by the crushers, for self-consume in their boilers, or sold in a restrict area; therefore, a significant potential of this solid biofuel is not being used actually in Portugal. Considering woody agricultural residues, the vineyard and olive tree are the main biomass producers, although the orchards of oranges, apple and pear also present a significant potential in Portugal.

Slovenia

Wood biomass is the most important renewable energy source in Slovenia. It is used for covering the heat demand in households, for the production of process heat in industry and for electricity production. The most commonly used wood fuel type in Slovenia is firewood, the use of wood chips and pellets is increasing rapidly. Slovenia is third the most forested country in Europe, with 58.3 % forests cover of the surface area; therefore the potential for the use of forest biomass is big.

Households are the largest wood fuel consumers with a total consumption of 1.600.000 tons of wood fuels recorded for 2015. Despite an increase in the domestic production of pellets, Slovenia remains a net importer of pellets. Annual production of wood pellets is 110.000 t, smaller manufacturers with a yearly production of under 10,000 t hold the greatest share. Production of wood chips is increasing each year, in last years it amounted to over 1.500.000 loose m3. The number of medium and high capacity wood chippers is approximately 200.

Spain

Industrial market

There are two main biofuels which are being used in the industrial market; the most used are the wood chips that are being used for thermal purposes but also in electric generation. The wood chips used in industrial market are around 3 Million DM tonnes. The second biofuel most used in industrial is olive cake, a by-product of the olive oil extraction with around 800.000 tDM/year potential.

There are also other kinds of wood chips coming from olive trees (prunings) or vineyards that may go to industrial use but in smaller quantities, the potential of these biomasses is huge and much more quantities could be destined to energy.

Domestic market

Regarding the domestic sector, the most used biomass is still the firewood with 1.500.000 tonnes/year as per official figures from MAGRAMA although actual quantities in the market are believed to be significantly bigger.

Wood pellets are the second biofuel most used for domestic. Nowadays are being consumed 443.925 tDM /year from which 406.542 are for domestic use (data from AVEBIOM for 2016). The use of this fuel is increasing very quickly and it has more than double in the last 3 -4 years. The number of producers has increased accordingly.

After wood pellets, the most used biomass for domestic is wood chips (240.000 tDM /year) which are mainly used in mid-size installations (50 – 500 kW). Also the use of this biofuel has been growing in the last years (in Spain there was 5 logistic centres in 2011 and around 16 in 2014). The prices has been more stable and reasonable since the mid-size installations are less affected by the mild winters and being much cheaper it is not so affected by the low price of fossil fuels.

In the case of Olive Stones, about 130.000 tDM /year are used every year in the domestic sector but as previously mentioned there are another 300.000 tDM /year that are now destined to the industrial sector but that could be destined to the domestic if they would be valorised (dried and screened).

Turkey

Turkey’s solid biomass market has a very high potential. However, upgrading the standards of this market requires that solid fuel standards be revised according to country-specific biomass. Both biomass stove producers and biomass fuel manufacturers are trying to collaborate against that problems.

In the 2nd BIOMASUDPLUS project workshop, it was observed that the market started to be very active. The awareness of our stakeholders has been seen to increase, and the opinions expressed by the stakeholders have been described to the authorities in order for the solid biomass market to function better.

Efforts are underway to encourage the use of more environmentally friendly solid biofuels instead of less environmentally friendly solid fuels used in the country, and to establish this biofuel chain in a healthy manner. As a result of the increase in public support, the solid biofuel market is expected to turn into a robust market cycle.